Related rules: F 2.1

Sponsored sales are defined as subscriptions or single issues purchased by a third party (sponsor) in quantities of 11 or more to promote the business interest of the sponsor. All sponsored-sale copies must be delivered to specific individual names at private residences or business offices and are intended for the personal consumption of the addressee. Copies purchased for distribution to schools are also included as paid sponsored copies. School copies may be purchased individually by the recipients or paid for by schools. The following sections outline the requirements for qualifying sponsored sales as paid circulation:

- Eligible Sponsors

- Payment

- Sponsored Notification to Recipient

- Contract Between Sponsor and Publication

- Digital Sponsored Copies

- Backup Documentation for AAM Audit

- What is Not a Sponsored Sale

- AAM Reporting

Eligible Sponsors

- Any business or organization whose primary activity is to sell or provide products or services to the public.

- The purchaser must be financially independent from the magazine.

- Copies purchased for distribution to schools and paid for by the school or funded through donations.

Examples of Eligible Sponsors:

- Retailers: In-person and online (for distribution to frequent buyers or high-value buyers)

- Charitable organizations (for distribution to their donors)

- Schools

Payment

- The sponsor has paid at least one cent, net of considerations, per subscription or single-copy sale.

Note: All consideration or inducement values must be subtracted from the purchase price to calculate the payment value (i.e., account credits, free or discounted products or services, etc.)

- Payment needs to be received within four months of start of service

- Proof of payment must be maintained for audit. Payment by the sponsor must be made to the publisher/agent within four months of the start of service.

Sponsored Payment Example:

A one-year ABC Motor Car subscription is given as a gift to customers who purchase tickets to the Chicago Auto Show. The Chicago Automobile Dealers Group agrees to pay $3.00 per subscription.

Sponsored Notification to Recipient

- The recipient of the magazine must be informed of the sponsor’s identity.

- Notification must occur at the beginning of service to the magazine.

- For subscriptions with a term of more than one year, a reminder notice must be sent to the recipient at least annually about why they are receiving the copy and who is sponsoring it.

- The notice must be clear and conspicuous, such as:

- Included on a sign, web page or flyer when the purchase is made.

- On an opt-in form.

- A separate notification (letter, postcard, etc.) may be sent to the consumer advising the recipient that they will receive a sponsored subscription, compliments of the purchaser.

- A sticker, flyer, wrap, banner, or similar item may be placed on the cover of the first copy of the magazine mailed to the individual.

Note: If the notification contains any information beyond the sponsor’s logo and contact information, AAM considers the additional information advertising. The sponsor is required to pay market value for this advertising above the cost of any magazine purchased.

Examples of Sponsored Notifications:

Notification Subscriptions:

“This magazine is compliments of…”

“You will receive a one-year subscription to Magazine X brought to you by…”

Notification Single Copy:

“This copy was sent to you by…”

Notification Via Address Label:

Compliments of XYZ Fashion Store

Mary Smith

123 Main Street

Notification Via Sticker on Magazine:

Enjoy this magazine, courtesy of

XYZ Fashion Store

20 South Street

Anytown, NY 12345

Notification Via Magazine Cover:

This magazine is provided to you by XYZ Fashion Store, located at 55 First Street, Anytown.

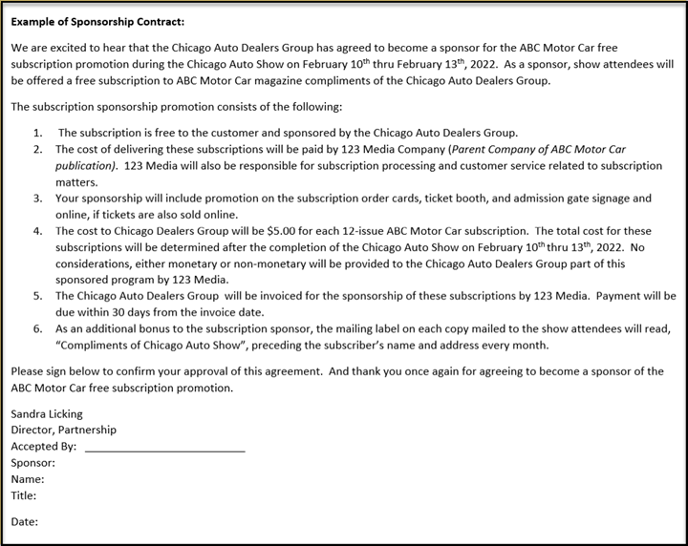

Contract between Sponsor and Publication

- A contract between the sponsor and the publication/agent for each magazine involved in the purchase must exist and include the following:

- Title of the magazine(s) involved

- Subscription quantities/single issues purchased

- Subscription term (or number of issues)

- Cost per subscription/single copy

- Total balance due

- Any other items received by the sponsor from the magazine, or its agent, related to the sponsored sale must be separately itemized in the contract or the invoice. This must include a charge to the sponsor for the market value of these items.

Example of Sponsorship Contract:

Digital Sponsored Copies

A digital issue is only eligible as a paid sponsored subscription or sponsored single copy if the consumer requests it and all other sponsored paid program requirements are met. In addition, the unique recipient must access the issue and the publisher must provide proof of access for the audit.

Backup Documentation for Audit

- Signed sponsored contract for each applicable sponsored program. The contract should include the following:

- Details of the sponsored initiative. (i.e., number of subscriptions/copies, duration of program and issues involved.)

- How the purchase was intended to promote the sponsor’s business interest.

- The price paid by the sponsored for each subscription/single issue.

- A statement affirming the transaction is “net” of all other considerations.

- Details on how the recipient is notified about the sponsored subscription/single issue. (i.e., cover wrap, insert card, address label, etc.)

- Proof of payment. Payment by the sponsor must be made to the publisher/agent within four months of the start date of service.

- An issue-by-issue breakdown on the publication’s circulation worksheet that includes all sponsored programs in the period.

What is Not a Sponsored Sale

The following types of distribution are not sponsored sales:

- Copies served to public place settings where copies are shared by multiple consumers.

- Copies delivered in bulk and picked up by unknown users, such as event distribution.

- Copies served in post-expiration status to sponsored subscriptions

- Back copies may not be used to fulfill sponsored sales distribution unless the recipient made a direct request (opted-in) for receipt of the publication.

Publishers may explore qualifying these copies as verified subscriptions or analyzed nonpaid bulk depending on the specific details of the program.

AAM Reporting

- Magazine subscriptions obtained through a sponsored program will be reported as Sponsored Subscriptions under Paid Subscriptions.

- You can optionally include a School Subscriptions Sold disclosure in the Notes section of the report that says:

- Included in sponsored sales is an average of __________ copies purchased by schools for student use.